What Are Options?

An option is a financial contract that gives you the right, but not the obligation, to buy or sell an underlying asset (usually a stock) at a predetermined price, on or before a specific date. You pay a fee called the premium to acquire this right.

Think of it like a reservation. If you pay $50 to reserve the right to buy a house at $300,000 anytime in the next 6 months, you have an option. If the house’s value rises to $350,000, your reservation is worth $50,000 — minus the $50 you paid. If the value drops, you simply walk away and lose only your $50 reservation fee. That is exactly how options work in the stock market.

Options exist for stocks, ETFs, indices (like the S&P 500), commodities, and currencies. In the US, one standard options contract controls 100 shares of the underlying stock. So when you see an option priced at $3.50, the actual cost is $3.50 × 100 = $350 per contract. This is a critical detail that every beginner must internalize before placing a trade.

Calls and Puts: The Two Types of Options

Every option is either a call or a put. There are no other types. Every strategy, no matter how complex, is built from combinations of these two building blocks.

Call Options

A call option gives you the right to buy the underlying stock at the strike price. You buy a call when you believe the stock price will go up.

Example: AAPL is trading at $180. You buy a $185 call option expiring in 30 days for $3.00 ($300 per contract). If AAPL rises to $195 before expiration, your call is worth at least $10.00 ($195 − $185 strike). Your profit: $10.00 − $3.00 paid = $7.00 per share = $700 per contract. That is a 233% return on your $300 investment. If AAPL stays below $185, you lose your $300 premium — that is your maximum loss, defined before you enter the trade.

Put Options

A put option gives you the right to sell the underlying stock at the strike price. You buy a put when you believe the stock price will go down, or when you want to protect (hedge) shares you already own.

Example: TSLA is trading at $250. You buy a $240 put option expiring in 30 days for $5.00 ($500 per contract). If TSLA drops to $220 before expiration, your put is worth at least $20.00 ($240 strike − $220). Your profit: $20.00 − $5.00 paid = $15.00 per share = $1,500 per contract. If TSLA stays above $240, you lose your $500 premium.

| Feature | Call Option | Put Option |

|---|---|---|

| Right granted | Buy the stock at strike price | Sell the stock at strike price |

| You profit when | Stock goes UP above strike + premium | Stock goes DOWN below strike − premium |

| Directional bias | Bullish | Bearish (or hedging) |

| Maximum loss (buyer) | Premium paid | Premium paid |

| Maximum profit (buyer) | Theoretically unlimited (stock can rise infinitely) | Substantial (stock can fall to $0) |

| Analogy | Security deposit to buy a house | Insurance policy on a stock you own |

The Five Essential Components of Every Option

Every options contract has five components. Understanding each is non-negotiable before placing a trade:

- Underlying Asset. The stock, ETF, or index the option is based on. “AAPL $185 call” means the option is based on Apple stock.

- Strike Price. The predetermined price at which you can buy (call) or sell (put) the underlying. It is the “target price” of the contract. A $185 call means you can buy at $185 regardless of where the stock is trading.

- Expiration Date. The date the contract expires. After this date, the option ceases to exist. You can have options expiring tomorrow (0DTE), this Friday (weekly), or months from now (monthly/quarterly). More time = more expensive premium.

- Premium. The price you pay to buy the option, or receive when selling one. This is the market price of the contract, determined by supply and demand, volatility, time remaining, and the distance between strike price and current stock price.

- Contract Size. In the US, one standard equity option contract = 100 shares. This multiplier applies to everything: premium, profit, loss. Always multiply the quoted price by 100 to get the actual dollar amount. Note that not all products behave identically at settlement — index options like SPX settle in cash while ETF and stock options result in share delivery. The complete breakdown of exercise style and settlement mechanics is in the Options Contract Specifications guide.

How Options Are Priced: Intrinsic and Extrinsic Value

Every option’s premium consists of two parts:

Option Premium = Intrinsic Value + Extrinsic Value (Time Value)

Intrinsic value is the real, tangible value of an option if you exercised it right now — the difference between the stock price and the strike price, but only when that difference is positive. A call on AAPL at $185 when the stock is at $190 has $5.00 of intrinsic value. A call at $195 when the stock is at $190 has zero intrinsic value because exercising it would mean buying at a higher price than the market.

Extrinsic value (also called time value) is everything in the premium beyond intrinsic value. Two forces drive it: time remaining (more time to expiration = more extrinsic value) and implied volatility (higher expected volatility = more extrinsic value, because the probability of a large move is priced in).

The key behavioral rule: extrinsic value decays to zero at expiration regardless of where the stock is trading. This decay — called theta decay — is the option buyer’s constant cost and the option seller’s primary income source. At-the-money options have the highest extrinsic value. Deep ITM and deep OTM options have the least. For the complete breakdown of how intrinsic value, extrinsic value, and moneyness interact — with worked examples across five strike zones — see the Options Moneyness guide.

Moneyness: ITM, ATM, and OTM

Moneyness describes the relationship between an option’s strike price and the current stock price. An option is in the money (ITM) when exercising it now would be profitable — stock above strike for calls, stock below strike for puts. It is at the money (ATM) when the strike is approximately equal to the stock price. It is out of the money (OTM) when exercising now would produce a loss — no intrinsic value remains.

For the complete treatment of moneyness — including the reversed call/put definitions, Greeks behavior by moneyness zone, the probability-cost tradeoff, and the deep OTM trap that destroys most beginner accounts — see the dedicated Options Moneyness: ITM, ATM, OTM guide. For practical trade decisions right now:

- Beginners buying options should generally start with ATM or slightly OTM strikes. They offer a balance between cost and probability of success.

- Deep OTM options (“cheap lotto tickets”) have very low probability of profit. They look cheap but rarely pay off — this is the most common beginner trap.

- If you are long an option: ITM is better (you are already making money). If you are short an option: OTM is better (the option expires worthless and you keep the premium).

Buying vs. Selling Options

Every options trade has two sides: a buyer and a seller. Their risk profiles are mirror images:

| Feature | Option Buyer (Long) | Option Seller (Short/Writer) |

|---|---|---|

| Pays/receives | Pays the premium | Receives the premium |

| Right/obligation | Has the right (no obligation) | Has the obligation (if buyer exercises) |

| Wants the stock to | Move significantly (in their direction) | Stay flat or move slightly against buyer |

| Time decay effect | Hurts (option loses value daily) | Helps (option loses value daily = profit) |

| Maximum loss | Premium paid (defined) | Potentially large or unlimited (naked calls) |

| Win rate | Lower (~30–40% for OTM buys) | Higher (~60–70% for OTM sells) |

| Best for beginners? | Yes — defined risk, simple execution | Only with defined-risk strategies (spreads) |

Key insight: Approximately 60–70% of options expire out of the money (worthless). This structural fact means sellers have a statistical edge — they win more often. However, when sellers lose, losses can be very large. Buyers lose small amounts often but can win big when a stock makes a significant move.

Start by buying options only (long calls and long puts). Your risk is defined: you can only lose the premium paid. Do not sell naked options until you have significant experience and understand margin requirements. If you want to sell options, start with defined-risk strategies like credit spreads, where your maximum loss is known before entry.

Beyond long calls and long puts, there are two additional fundamental positions — the short call and the short put — each with a distinct risk profile, Greek signature, and market outlook. The complete mechanics of all four positions, including P&L by price scenario and the five-question decision tree for selecting which to use, are in the Four Option Positions guide.

Your First Options Trade: Step by Step

Here is the exact process for placing your first options trade, using a long call as the example:

Step 1: Form a Directional Thesis

Before buying an option, you need a reason. “I think AAPL will go up” is not enough. A proper thesis includes: direction (up), magnitude (by how much — e.g., to $195+), and timeframe (by when — e.g., within 30 days). The timeframe determines your expiration date. The magnitude determines your strike price.

Step 2: Choose Expiration

As a beginner, give yourself more time than you think you need. If you expect a move within 2 weeks, buy a 30–45 day option. This extra time buffer protects against theta decay and gives your trade room to work. Avoid 0DTE and weekly options until you are experienced — they decay at extreme rates and a 1% move in the wrong direction can destroy 50% of a weekly option’s value within hours. Once you are ready to explore same-day expirations, the complete framework is in the 0DTE Options guide.

Step 3: Choose Strike Price

For your first trades, use ATM or slightly OTM strikes (1–2 strikes above the current price for calls, 1–2 below for puts). These offer a reasonable balance of cost and probability. Avoid deep OTM “lotto” strikes — the probability of profit is very low.

Step 4: Check Liquidity

Before buying, verify that the option has sufficient volume and open interest. Look for:

- Open interest > 500 contracts at your strike

- Bid-ask spread < 10% of the option’s price (e.g., if the option is $3.00, the spread should be $0.30 or less)

- Volume > 100 contracts/day at your strike

Low liquidity means wide bid-ask spreads, which eat into your profits before the trade even begins. Stick to liquid underlyings (AAPL, MSFT, SPY, QQQ, TSLA, AMZN, NVDA) for your first trades. What volume and open interest actually measure — and why their combination tells a very different story than either metric alone — is covered in the Open Interest vs. Volume guide. For a practical walkthrough of reading every column in the options chain, see How to Read an Options Chain.

Step 5: Size Your Position

Never risk more than 1–3% of your account on a single options trade. If your account is $5,000, your maximum risk per trade is $50–$150. Since the premium is your maximum loss when buying options, simply ensure the contract cost stays within this range. Start with 1 contract.

Step 6: Place the Order

Use a limit order, not a market order. Set your limit price at or near the mid-price (the midpoint between bid and ask). Market orders on options can result in terrible fills due to wide spreads. Be patient — if your limit isn’t filled immediately, wait or adjust by $0.05 increments.

Managing Your Trade

Entering a trade is the easy part. Managing it is where most beginners fail.

Set Exit Rules Before Entry

Before placing any trade, define two exit points:

- Profit target: “I will sell when the option doubles in value (100% gain).” Or: “I will sell when the stock reaches $195.” Having a target prevents greed from turning a winner into a loser.

- Stop loss: “I will sell if the option loses 50% of its value.” This preserves capital for the next trade. Do not hold until expiration hoping for a miracle — theta decay will destroy the remaining value.

The 50/21 Rule for Beginners

A simple, effective management framework:

- Take profits at 50% gain. If you bought at $3.00, sell at $4.50. This sounds conservative, but taking consistent 50% gains accumulates faster than waiting for home runs that rarely materialize.

- Close with 21 days to expiration (DTE). Theta decay accelerates dramatically in the final 21 days. Even if your trade is profitable, close it before the 21-DTE mark and re-enter a new position with more time if you still have conviction.

The 10 Most Common Beginner Mistakes

- Buying deep OTM options (“lotto tickets”). They are cheap for a reason — the probability of profit is often below 10%. The expected value is negative. You will lose money more often than you win, and the wins rarely compensate for the cumulative losses.

- Ignoring time decay (theta). Every day you hold an option, it loses value even if the stock doesn’t move. This especially hurts OTM options in the final 21 days before expiration. Time is the option buyer’s greatest enemy.

- Buying too short-dated options. Weeklies and 0DTE options look cheap but decay at extreme rates. Give yourself at least 30–45 DTE as a beginner.

- Not checking liquidity. Trading illiquid options means paying wide bid-ask spreads — you lose money the moment you enter. Only trade options with open interest > 500 and tight spreads.

- Oversizing positions. Risking 10–20% of your account on a single options trade is a path to account destruction. One bad trade can wipe weeks of gains. The 1–3% rule exists for a reason.

- Not having an exit plan. Entering without predefined profit targets and stop losses means emotional decision-making. Set your exits before you enter. No exceptions.

- Holding through earnings without understanding IV crush. Implied volatility inflates before earnings announcements, making options expensive. After the announcement, IV collapses (“IV crush”), destroying extrinsic value. Even if you predict the direction correctly, IV crush can turn your trade into a loss.

- Forgetting the contract multiplier. An option at $3.50 costs $350, not $3.50. A $0.50 loss per share is $50 per contract. Always multiply by 100.

- Selling naked options without understanding the risk. Selling a naked call has theoretically unlimited risk. Selling a naked put risks the full strike price × 100. Beginners should never sell naked options — use defined-risk strategies only.

- Trading without education. Options respond to direction, time, volatility, and interest rates simultaneously. Invest time in learning before investing money in trading. The library below is your structured path forward.

Your Learning Path Through the StrikeWatch Lab

This guide covered the foundation. Every article below builds directly on what you learned here. Work through them in order — each one unlocks the next.

Foundation: How Options Work

- Options Moneyness: ITM, ATM, OTM — The complete treatment of how strike price relates to stock price, how Greeks behave differently across moneyness zones, and why cheap deep OTM options are the most common source of beginner losses.

- The Four Option Positions — Long call, short put, long put, short call: their P&L by price scenario, Greek profiles, and a five-question framework for choosing which position fits your market view.

- Options Contract Specifications: American vs. European — Why SPX and SPY track the same index but behave completely differently at settlement. Early assignment risk, AM vs. PM settlement, cash vs. physical delivery — essential before you sell your first option.

Reading the Market: Data and Structure

- Open Interest vs. Volume Explained — What each metric measures, why their combination tells you whether new money is entering or existing positions are closing, and how high OI creates structural support and resistance through dealer hedging.

- How to Read an Options Chain — Every column decoded: bid, ask, volume, open interest, IV, and Greeks. The V/OI ratio as an anomaly detector. A six-step strike selection process using real chain data.

- Put/Call Ratio: Reading Sentiment and Positioning — How to use the PCR as a contrarian indicator, the difference between volume PCR and OI PCR, and how PCR term structure reveals whether fear is event-specific or structural.

Volatility: The Force Behind Every Option Price

- Implied vs. Historical Volatility — What IV and HV measure, why they diverge, the IV–HV spread as a strategy-selection filter, and how IV Rank and IV Percentile tell you whether options are cheap or expensive right now.

- The Expected Move — How to calculate the market’s implied price range for any period, use it for strike selection, and integrate it with GEX structural levels.

- VIX Explained — How the “fear index” is constructed, what VIX levels mean for options pricing, and how the VIX term structure reveals whether the market is pricing a short-term event or a structural regime shift.

- IV Surface, Skew, and Term Structure — How implied volatility varies across strikes and expirations simultaneously, and how to read the full volatility surface as a risk map.

Market Structure: Where Price is Drawn and Repelled

- Max Pain Theory — Why options prices tend to gravitate toward the strike where option writers pay the least at expiration, how dealer delta-hedging creates this gravitational pull, and when Max Pain reliably predicts expiration price versus when it fails.

- Dealer Hedging Regimes: GEX and the Zero Gamma Level — How aggregate dealer gamma positioning determines whether price moves are dampened (positive GEX) or amplified (negative GEX), and how the Zero Gamma Level marks the regime boundary.

Institutional Flow: Reading Where Smart Money Moves

- Options Order Flow & Market Maker Positioning — How to read the tape like an institution: aggressor side, strike intelligence, hedging vs. speculative flow classification, roll detection, and how dealer hedging transmits institutional positioning directly into price.

- Unusual Options Activity: Detection & Trading — The sweep/block/golden sweep taxonomy, the five-signal diagnostic table, three context filters for validating institutional flow, and the execution framework for following high-conviction prints.

- Options Flow Intelligence: The Complete Framework — How open interest, active volume, and tape aggression integrate into a single analytical system. The four flow regime archetypes, the GEX confirmation matrix, and the pre-trade checklist.

Strategy: Applying the Framework

- 0DTE Options: The Complete Strategy Guide — Why gamma is 50× larger on same-day expirations, eight strategies mapped to GEX regimes, the dealer-aware scalp, and why never selling premium in a negative GEX regime is the single most important 0DTE risk management rule.

- Position Sizing Around GEX and Volume Floors — How to scale position size to the current GEX regime, use volume profile floors as stop-level anchors, and implement drawdown controls that keep losses recoverable.

Advanced: Quantitative and Systematic Approaches

- Variance Risk Premium: Systematic Trading Guide — Why implied volatility overstates realized volatility 85% of the time, how to build a systematic short-vol framework with explicit regime filters, and the backtestable SPX iron condor ruleset.

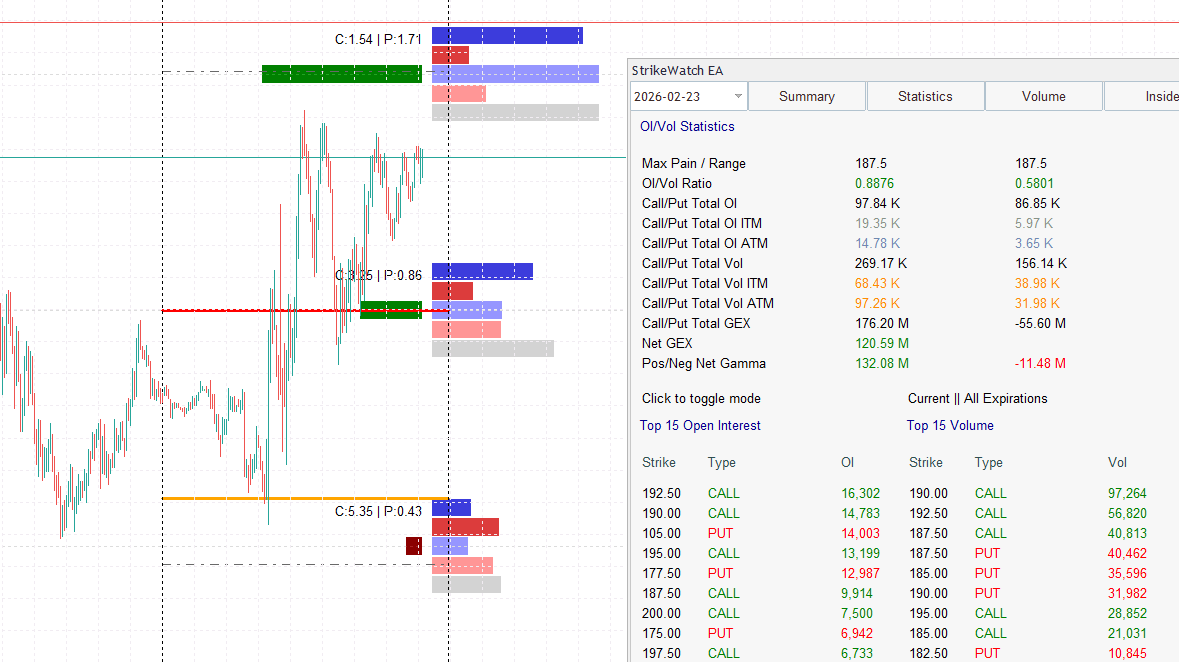

For hands-on application of these concepts directly inside MetaTrader 5, StrikeWatch EA provides real-time GEX, Max Pain, Expected Move, IV Surface, and OI/Volume data — all overlaid on your chart so you can act on institutional-grade analytics without leaving your trading environment.