The Most Persistent Edge in Finance: Edge and Trap

If you could access only one piece of information before trading options, it should be this: implied volatility overstates realized volatility approximately 85% of the time. This is not a temporary anomaly or a statistical artifact. Decades of empirical research show that equity index options — and many single-stock options — trade with implied volatility that is on average higher than subsequent realized volatility.

The Variance Risk Premium (VRP) — defined as the difference between implied variance and subsequently realized variance — has been extensively documented in academic literature. Carr and Wu (2009) analyzed S&P 500 options data and found that the VRP is negative on average for option buyers (investors pay more for variance protection than they receive in realized variance), economically large, and time-varying. Research from the Copenhagen Business School (2021) confirmed that the VRP averages 2–4 volatility points for the S&P 500 — meaning if implied volatility is 20%, realized volatility tends to come in around 16–18%. This excess is structurally related to the persistent gap between Implied and Historical Volatility — for the complete mechanics of why the premium exists, including the three institutional demand pillars that sustain it permanently, see that foundational guide.

Selling options to harvest this premium is the foundation upon which the entire institutional options selling industry is built. But while the edge is real, it is also asymmetric: small, frequent gains punctuated by occasional large losses if risk is not explicitly controlled. A robust short-vol system must therefore be selective, diversified, and regime-aware. The rest of this article builds that system.

Measuring the VRP: The IV–HV Spread as Entry Filter

The primary proxy for the VRP is the IV–HV spread — the difference between current implied volatility and trailing realized (historical) volatility. The complete mechanics of this spread, the direction table linking spread magnitude to strategy selection, and the three structural pillars that make it a durable edge are covered in the Implied vs. Historical Volatility guide. To normalize the raw spread across different volatility regimes, two contextual metrics are required: IV Rank (IVR) and IV Percentile (IVP) — for the complete formulas, the four-combination divergence matrix, and the five-step screening workflow with multi-stock examples, see IV Rank vs. IV Percentile: Screening Workflow and Divergence Guide. For this system, treat all three metrics as pre-qualified inputs: the regime filter logic and structural overlays that determine when to act on them are the subject of the sections that follow.

Index vs. Single-Name Short-Vol Universes

VRP is most robust in index options (SPX/NDX and ETF analogues like SPY/QQQ), where diversification and structural hedging demand create persistent, reliable premiums. Single-stock options also exhibit VRP, but they come with unique challenges:

- Higher idiosyncratic jump risk (earnings, M&A, regulatory events).

- More volatile and fragmented VRP patterns over time.

A systematic short-vol universe should therefore be constructed as:

- Core (70–80%): Broad index products (SPX/ES, NDX/NQ, large ETFs) where the VRP is most stable and jump risk is minimized through broad diversification.

- Satellite (20–30%): Selected large-cap, highly liquid single names with well-behaved volatility profiles — strictly traded outside of their earnings windows.

Harvesting Strategies: From Institutional to Defined-Risk

The VRP can be captured through a spectrum of strategies, each balancing premium collection with tail risk:

Institutional Approaches

- Variance Swaps: The purest instrument for VRP exposure. A variance swap pays the difference between realized variance and a fixed strike. They are market-neutral by construction but carry convexity risk: losses accelerate non-linearly when realized variance significantly exceeds the strike.

- Delta-Hedged Short Straddles: Sell ATM straddles and continuously delta-hedge the position. This isolates the pure volatility bet: you profit if realized volatility is less than the implied volatility you sold. Research from Imperial College London shows this effectively captures the VRP under normal conditions but generates extremely large tail losses during jumps.

- Systematic Put Writing: The simplest directional harvest (e.g., selling 30-day puts at 5% OTM). The CBOE PUT Index demonstrates equity-like returns with lower volatility historically. However, it blends VRP with directional equity exposure, suffering during market crashes.

Retail & Systematic Quant Structures

For independent traders, short-vol systems typically rely on defined-risk spreads to align margin with economic risk and cap tail exposure:

| Structure | Use Case | Pros | Cons |

|---|---|---|---|

| Short Vertical Spreads | Directional or mildly directional short vol on index or stock. | Defined max loss; simple; tunable width. | Caps payoff even if realized vol drops significantly below implied. |

| Iron Condors | Range-bound, mean-reverting regimes. | Defined risk on both sides; monetizes VRP in both tails simultaneously. | More legs to manage; sensitive to outlier directional moves if wings are too narrow. |

| Short Strangles (with tail hedges) | Advanced users seeking higher VRP capture. | Higher premium collection; wide breakevens. | Large tail risk; requires strict overlays like VIX calls or deep OTM index puts. |

Spread width controls the trade-off between premium and maximum loss. System design should explicitly parameterize width relative to the Expected Move and the current volatility regime.

When the VRP Inverts: Regime Filters & Structural Warning Signs

VRP filters alone are not enough. The VRP is not always positive. During extreme market stress, realized volatility can temporarily exceed implied volatility — the insurance claims exceed the premiums. These VRP inversions are rare (occurring roughly 15% of trading days) but devastating. Van Tassel (2022) found that during crisis episodes, realized variance shocks dominate implied expectations, causing the VRP to invert.

To prevent system destruction, quantitative traders use structural microstructure filters — specifically GEX (Gamma Exposure), the Zero Gamma Level (ZGL), and Max Pain — to detect regime shifts before or as they happen. The complete mechanics of how dealer gamma positioning creates stabilizing and destabilizing regimes are covered in the Dealer Hedging Regimes & GEX guide. For the purposes of the VRP system, the actionable signal set is:

- HV exceeding IV for 3+ consecutive sessions: The options market has not yet repriced to reflect the new, aggressive volatility regime. This is the most dangerous phase for premium sellers.

- Strong positive GEX, price well above ZGL: Dealer hedging is stabilizing (buying dips, selling rips); intraday ranges tend to be compressed. Short-vol strategies are structurally favored.

- Price near ZGL or in negative GEX: When the underlying breaks below the Zero Gamma Level, dealer hedging shifts from stabilizing to amplifying (selling into weakness). Realized volatility mechanically expands, often exceeding the implied volatility that was priced in before the break. Short-vol systems should immediately reduce size or turn off.

- VIX term structure backwardation: When front-month VIX futures trade above back-month, the market is pricing in more risk now than later — consistent with a VRP inversion. For the complete VIX term structure framework, including the contango/backwardation mechanics and the backwardation-to-contango re-entry signal, see the VIX: The Fear Index guide.

- Max Pain clusters: When price oscillates near strong Max Pain strikes with positive GEX, mean reversion and pinning are highly likely into OPEX, heavily favoring range-bound short-vol structures like Iron Condors.

System Design: Entry, Exit and Strategy Selection Rules

The IV–HV spread and regime metrics must be woven into explicit, systematic rules dictating not just if you trade, but what you trade.

Strategy Selection Based on IV–HV

- Wide positive spread (IV ≫ HV), IV Rank > 50%: Premium selling environment. Short strangles, iron condors, jade lizards, and credit spreads. Theta is your ally; the market is overpricing risk.

- Narrow spread (IV ≈ HV), IV Rank 20–50%: Neutral zone. No strong VRP edge. Prefer directional trades with defined risk (debit spreads) where the vol component is not the primary profit driver.

- Negative spread (HV > IV), IV Rank < 20%: Premium buying environment. Long straddles/strangles or calendar spreads. The market is underpricing current realized risk — gamma buyers have the edge.

Trade Execution Rules

- Expiry selection: Commonly 30–60 DTE for indices, 20–45 DTE for single names outside earnings, balancing favorable theta decay vs. gamma risk.

- Strike selection: OTM short strikes placed near but outside the mathematically Expected Move; long wings set wider than typical stress moves.

- Profit-taking: Mechanical rules, such as closing at 40–50% of maximum profit, or taking time-based exits if the VRP has been rapidly realized early in the trade.

- Stop-losses: Delta-based (e.g., closing if the short option delta doubles or exceeds 0.30) or structural (e.g., exiting immediately if price crosses below the ZGL).

Drawdown Management and System Kill-Switches

Because short-vol strategies can experience clustered losses during violent regime shifts, the system must include explicit, non-negotiable drawdown controls. The full position-sizing framework — including the GEX-scaled sizing model, NLV-based risk limits, and volume floor anchoring — is in the Position Sizing Around GEX and Volume Floors guide. For the VRP system specifically, four kill-switches are non-negotiable:

- Max per-trade loss: Strict position sizing. E.g., max 0.5–1% of Net Liquidating Value (NLV) at risk per spread. Close or roll when the loss reaches a fixed multiple of the initial premium collected.

- Daily/weekly loss limits: Stop opening new short-vol trades for the day/week when realized losses exceed a specific portfolio threshold (e.g., 3% NLV).

- Equity curve stop: Pause or completely de-risk the system if the peak-to-trough portfolio drawdown exceeds a pre-set limit (e.g., 10–15%).

- Regime kill-switch: Turn the short-vol system off automatically when structural metrics indicate crisis conditions: net negative GEX, price below ZGL, or severe VIX backwardation.

Example: Index Iron Condor System

As a concrete illustration of a backtestable quantitative framework, consider this SPX Iron Condor system ruleset:

- Universe: SPX index options.

- DTE (Days to Expiration): 30–45 DTE entries.

- Entry Filter: IVR between 30–70; IV > HV by at least 3–5 vol points; SPX price > 3% above ZGL; Net GEX must be positive across the short-strike region.

- Structure: Short put and short call placed at 1.0–1.2 × Expected Move OTM. Long wings placed 2.0–2.5 × Expected Move OTM.

- Management: Take profits at 40–50% of maximum credit received. Cut losses if either short strike delta exceeds 0.30 or if SPX price crosses below the ZGL.

- Risk Controls: Max 1% NLV risk per condor structure. Daily loss limit of 3% NLV. System fully disabled if a 10% portfolio drawdown is hit or GEX flips negative while IVR spikes.

Robust backtests for such systems must always include full crisis periods (2008, 2018 Q4, March 2020), realistically model bid-ask spread slippage, and utilize out-of-sample validation to avoid overfitting.

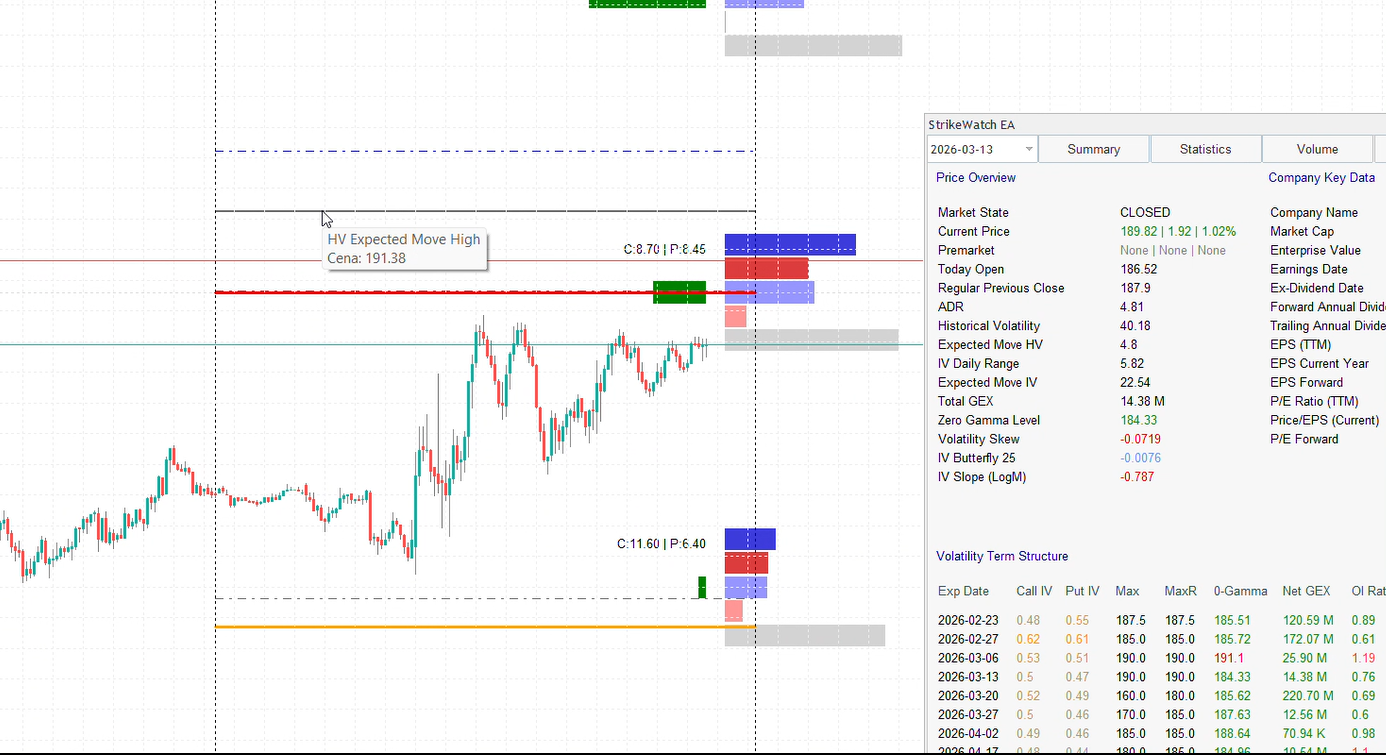

Systematic Short-Vol in StrikeWatch EA

StrikeWatch EA equips you with the exact information architecture needed to measure, monitor, and run systematic VRP strategies like a professional desk directly in MT5:

- Summary Surface (IV vs. HV Dashboard): Real-time comparison of implied and historical volatility. The raw spread, IV Rank, and IV Percentile are calculated automatically. For the complete interpretation framework, see Implied vs. Historical Volatility and IV Rank vs. IV Percentile.

- Dual Expected Move: Separate projections based on IV (what the market prices) and HV (what is actively happening). When the IV-based move is significantly wider, the VRP is rich.

- Volatility Regime Detection: The GEX Profile and ZGL overlays map the structural gamma regime, distinguishing between stabilizing (safe to sell) and destabilizing (dangerous) environments.

- Strike-Level Intelligence: Max Pain and OI/Volume histograms help visualize liquidity and congestion zones to place short strikes intelligently behind structural “walls.”

- Portfolio Greeks: Aggregate portfolio gamma, theta, and vega tracking ensures system-level short-vol exposures remain well within your defined risk limits.

When combined with clear rules, drawdown constraints, and disciplined execution, these tools allow you to harvest the Volatility Risk Premium as a deliberate, systematic strategy rather than a hidden, accidental bet.

The VRP is real, persistent, and structural — but not unconditional.

IV overstates realized volatility ~85% of the time and by 2–4 vol points on

average for the S&P 500. The three institutional pillars sustaining it are covered

in Implied vs. Historical

Volatility.

Universe construction determines system robustness. Core (70–80%)

index products provide the most stable VRP harvest. Satellite single names (20–30%)

add yield but require earnings exclusion and stricter regime filters.

Strategy selection is a function of IV–HV spread magnitude.

IV ≫ HV → iron condors and short strangles. IV ≈ HV → directional

debit spreads. HV > IV → long vol. For the operational screening workflow

using IVR and IVP, see

IV Rank vs. IV

Percentile.

The VRP inverts ~15% of the time — and those episodes are

catastrophic. GEX regime (positive vs. negative, ZGL position) and VIX term

structure (contango vs. backwardation) are the two non-negotiable structural filters

before any short-vol entry.

The kill-switch is not optional. Net negative GEX, price below ZGL,

or severe VIX backwardation — any one of these turns the system off. No VRP

signal overrides a structural crisis regime.

The SPX Iron Condor ruleset in Section 8 is the template. Entry filter

(IVR 30–70, IV > HV by 3–5pts, price >3% above ZGL, positive GEX),

structure (1.0–1.2× EM short strikes, 2.0–2.5× EM wings),

management (50% profit target, delta stop at 0.30, ZGL structural stop), and risk

controls (1% NLV max, 3% daily loss limit, 10% drawdown kill-switch).