Execution Quality: The Hidden Lever in Options Performance

Most options education focuses on payoffs and probabilities. Very little is said about the microstructure layer where trades actually fill: bid-ask spreads, displayed vs hidden size, order types and matching rules. Yet for active options traders, this layer is where much of the real edge is won or lost.

Options markets are fragmented, thin away from the most popular strikes, and heavily influenced by market-making algorithms. Entering a multi-leg spread with the wrong order type, at the wrong moment in the wrong part of the liquidity profile, can easily cost more than the entire expected value of the trade. This article explains how to use order types, time-in-force instructions and StrikeWatch’s structural analytics to reduce slippage and align execution with dealer and institutional flow.

This article covers the execution mechanics layer of options microstructure: how to fill trades with minimal slippage and maximum structural alignment. For the layer that precedes execution — reading the tape to understand who is trading and how dealers are positioned before you place your order — see Options Order Flow & Market Maker Positioning. For the structural sizing layer that governs how much capital to deploy around GEX and volume floors before you even choose an order type, see Margin and Buying Power: Sizing Around GEX and Volume Floors.

Bid-Ask Spreads, Liquidity and Slippage in Options

The bid-ask spread is the most visible measure of transaction cost. In options, spreads widen when:

- Liquidity is low (few market participants quoting meaningful size).

- Volatility is high and market makers face larger hedging risk.

- Contracts are far OTM, deep ITM or very close to expiry, making fair value more uncertain.

For a single-leg trade, hitting the ask and lifting the offer may not look disastrous. But in multi-leg strategies (verticals, iron condors, butterflies), slippage accumulates on every leg. Paying the full spread on each side can turn a structurally positive-EV trade into a negative-EV one before the position even leaves the order book. The full framework for reading bid-ask columns, displayed size and IV columns in an options chain before placing an order is in How to Read an Options Chain: Volume, OI, Bid-Ask & Greeks.

In practice, your execution goal is simple: capture as much of the bid-ask spread as possible by working limit orders near the mid-price, at times and levels where genuine liquidity exists.

Core Order Types: Market, Limit, Stop and Stop-Limit

Most brokers expose the same fundamental order types for options as for stocks. Their behavior is straightforward, but their consequences in illiquid options markets are often underestimated.

| Order Type | Behavior | Best Use | Risks |

|---|---|---|---|

| Market | Executes immediately at the best available prices until filled. | Highly liquid, tight-spread options; urgent exits in stressed markets. | Unbounded price; can fill far from mid in wide or gapping markets. |

| Limit | Executes only at your price or better; remainder rests in the book. | Default choice for opening and closing options in most conditions. | May not fill in fast markets or if price never trades through your limit. |

| Stop | Triggers a market order once a stop price is touched. | Simple protection when liquidity is deep and spreads are modest. | Stop can trigger in a gap and fill at a much worse price than expected. |

| Stop-limit | Triggers a limit order once a stop price is touched. | Controlled exits in volatile or thin markets. | Order can trigger but never fill if price jumps through the limit. |

As a rule of thumb, professionals avoid pure market orders in options except in the most liquid, tight-spread underlyings or when exiting a position that has already gone badly wrong and must be flattened immediately.

Time-in-Force: IOC, FOK and GTC in Options Execution

Time-in-force instructions control how long your order lives and what happens if it cannot be filled immediately. Three are particularly relevant in options:

- Day / GTC (Good-Till-Canceled): The order rests in the book until filled or canceled (day) or indefinitely (GTC), providing passive liquidity at your limit price.

- IOC (Immediate-or-Cancel): The order must be executed immediately for all or part of the quantity; any unfilled remainder is canceled without entering the book.

- FOK (Fill-or-Kill): The order must be executed immediately and in full or not at all; partial fills are not allowed.

IOC is useful when you want to probe available liquidity at a given price without leaving residual orders exposed. FOK is appropriate when partial fills would be structurally undesirable — for example, opening only one leg of a complex spread.

Single-Leg vs Multi-Leg Execution: When to Use Combos

Multi-leg strategies add another layer of execution risk: the danger of being filled on one leg but not the others, especially in fast markets. Where your platform and broker allow it, using combination (multi-leg) orders is generally superior to legging manually.

| Approach | Description | Advantages | Trade-Offs |

|---|---|---|---|

| Single-leg orders | Enter/exit each option leg separately. | Maximum flexibility, possible price improvement on individual legs. | Leg risk; can end up unintentionally directional or naked. |

| Combo order | All legs submitted as one structure with a net price. | No partial-leg risk; guarantees structure is opened/closed as designed. | Fill depends on aggregate liquidity; less granular control per strike. |

| IOC/FOK combo | Combo order with IOC/FOK time-in-force. | Ensures you either get the full spread or nothing. | More likely to miss fills in thin or fast markets. |

For defined-risk spreads (verticals, iron condors, butterflies), using combo orders at a sensible limit price relative to the mid is typically the cleanest execution method. It lets you focus on structure and risk, not on juggling partially filled legs. The framework for choosing which spread structure to use at which market stage is in Options Strategies for Income Generation.

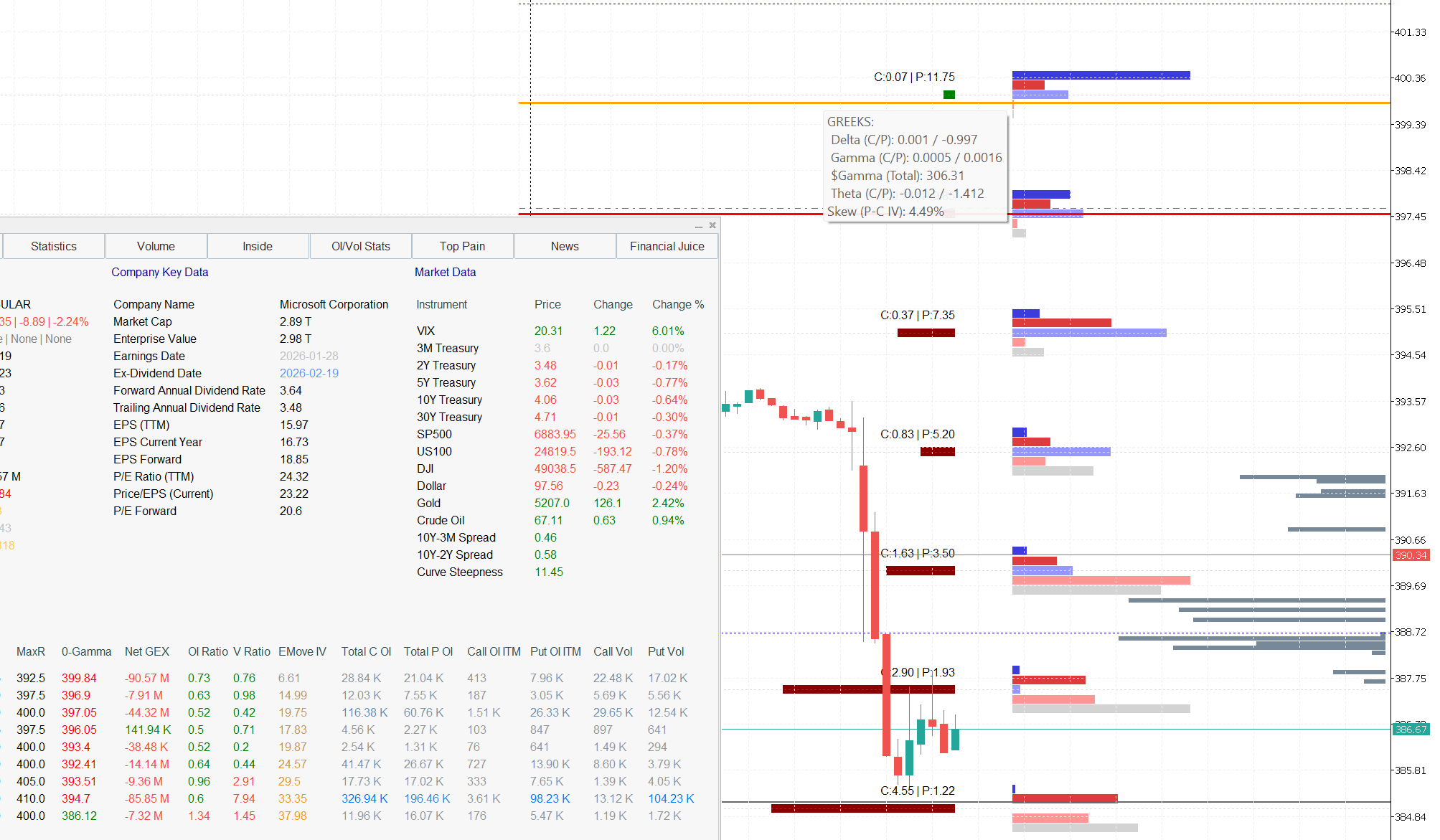

Anchoring Execution to GEX, Max Pain and ZGL

StrikeWatch adds a structural dimension rarely seen in retail platforms: Gamma Exposure (GEX), the Zero Gamma Level (ZGL) and Max Pain overlays. These are not just ideas for directional trades — they are also execution anchors. The full mechanics of why GEX and ZGL behave as structural magnets and how dealer gamma creates stabilizing vs amplifying regimes are in Dealer Hedging Regimes: GEX and Zero Gamma Level.

- GEX peaks and walls: Areas with large positive GEX often act as magnets and stabilization zones; negative GEX pockets can see air-pocket moves. Executing near positive GEX peaks tends to offer deeper two-sided liquidity.

- Zero Gamma Level (ZGL): The flip line between stabilizing and destabilizing dealer hedging. Around this level, liquidity can evaporate quickly as regimes shift. Treat ZGL as a zone of elevated slippage risk for market orders.

- Max Pain strike: The price level where option sellers maximize P&L at expiration, often associated with large OI clusters and dealer gamma interest. The mechanics of why Max Pain creates structural gravity — particularly in the final days before expiration — are in Max Pain Theory: How Market Makers Pin Options Strikes at Expiration.

Practical implications for order placement:

- When opening positions, prefer limit orders executed near GEX walls, Max Pain magnets or durable volume nodes rather than in the middle of thin regions between them.

- Avoid chasing trades with market orders as price slices through ZGL into negative gamma. Slippage risk is highest there.

- For exits, anticipate structural magnets: if Max Pain sits just above your current price into OPEX, you may get better fills by working limits closer to that level rather than panicking into a transient dip.

Reading OI/Volume Histograms and Volume Profiles for Liquidity

StrikeWatch’s OI & Flows and Volume modules give you a real-time picture of where institutional participants are active. Three data layers are relevant for execution quality:

- OI histograms: Show strikes where large open interest is concentrated. These are often where market makers quote tightest spreads and deepest size. The full distinction between OI as a stock of risk vs volume as a flow of risk, including the four-scenario matrix for reading OI/Vol together, is in Open Interest vs. Volume in Options: What They Mean and How to Use Both.

- Volume histograms: Highlight which strikes have traded heavily in the current session, revealing intraday liquidity hot-spots.

- Volume profiles on price: Show where the underlying has transacted most over the chosen lookback — true volume floors (High-Volume Nodes, HVNs) and low-liquidity zones (Low-Volume Nodes, LVNs or gullies). The full Auction Market Theory framework behind POC, Value Area, HVN/LVN classification and Liquidity Density is in Volume Profile, Auction Market Theory and Liquidity Density. For execution purposes, the key rule is simple: execute at or near HVNs; avoid market orders in LVNs.

Execution playbook:

- Prefer entering and exiting at strikes where both OI and intraday volume are elevated. This is where institutional flow and dealer interest are highest.

- Avoid far-from-the-money strikes with thin OI/Vol unless you are fully prepared for wide spreads and partial fills.

- Combine strike-level liquidity with price-level volume floors on the underlying: executing near a major HVN reduces impact and improves the odds of multiple participants competing for your order.

Execution Strategy in MT5 with StrikeWatch: A Step-by-Step Workflow

Here is a practical workflow for entering and exiting options structures on MT5 using StrikeWatch as your execution compass:

- Identify the structural context: Check GEX, ZGL and Max Pain overlays around the current price. Note whether the regime is positive or negative gamma and how close spot is to ZGL. Full regime classification in Dealer Hedging Regimes: GEX and ZGL.

- Scan OI & Flows: Find strikes and expirations with high OI and volume that align with your directional or income thesis. Avoid orphaned strikes with poor liquidity. For reading aggressor-side volume and identifying institutional intent before execution, see Options Order Flow & Market Maker Positioning.

- Check Volume module: Confirm that the underlying is trading near a volume floor (HVN) rather than in a thin liquidity gulf (LVN). Deep nodes are better execution zones. POC, Value Area and HVN/LVN methodology in Volume Profile and Auction Market Theory.

- Choose the right structure and order type: For spreads, use combo limit orders at or near the mid-price; for single-leg exits in fast markets, consider tighter limits or IOC instructions.

- Set realistic limits: Start near mid or slightly inside the spread; if activity is high and book depth is good, you can edge toward the bid (for sells) or ask (for buys) over time.

- Use IOC/FOK sparingly: Deploy IOC or FOK when you must avoid partial fills, such as entering large spreads in thin markets. Be prepared for more unfilled attempts.

This process may sound elaborate, but in practice it becomes a fast visual check: structural regime → strike-level liquidity → price-level volume floor → appropriate order type and limit.

Common Execution Errors and How to Avoid Them

Most options traders eventually learn the hard way that good ideas are not enough. The most common execution mistakes include:

- Using market orders by default: Particularly dangerous in wide-spread, low-volume or negative-gamma conditions.

- Legging into complex structures in fast markets: Opening one side of an iron condor or butterfly, then failing to fill the other side as prices move.

- Ignoring time-in-force: Leaving stale GTC orders sitting in the book where they can be picked off during overnight gaps or illiquid conditions.

- Trading at structurally bad levels: Chasing fills in the middle of low-volume gullies (LVNs), far from GEX walls and Max Pain magnets.

- Ignoring slippage in position sizing: Treating expected slippage as zero when calculating whether a trade meets your 1–2% risk budget. In thin options markets, round-trip slippage on both legs can equal 0.3–0.5% of portfolio value on its own. Always size as if you will pay the full spread on every leg. The full position sizing framework is in Options Risk Management and Position Sizing Guide.

- Executing into expiration-week pinning zones with market orders: In the final days before expiry, price gravitates toward high-OI strikes (pin risk). Market orders inside the pin zone are particularly expensive because dealer gamma hedging creates rapid, oscillating price action with wide effective spreads. Use limit orders inside the pin or work limits toward the Max Pain strike instead. Pin risk mechanics in Options Expiration Cycle, OPEX and Pin Risk.

All of these can be mitigated by a disciplined combination of limit orders, appropriate time-in-force, and the structural context provided by StrikeWatch’s analytics.

Execution Edge in StrikeWatch EA

StrikeWatch EA is more than a visualization tool for macro options concepts. Used properly, it is an execution edge:

- GEX and ZGL: Tell you when to be aggressive (positive gamma, far from ZGL) and when to be conservative (near or below ZGL). Full regime mechanics in Dealer Hedging Regimes: GEX and Zero Gamma Level.

- Max Pain and OI/Vol histograms: Point you to strikes where dealer and institutional interest is highest and spreads tend to be tightest. OI lifecycle and how OI concentration creates structural levels in Open Interest vs. Volume in Options.

- Volume profiles: Show you where the underlying’s order book is deepest, so you can place entries and exits into actual demand and supply rather than empty air. Full POC/HVN/LVN methodology in Volume Profile and Auction Market Theory.

- OI & Flows tape: Shows the last 30 largest options prints with aggressor-side classification, so you can read the directional intent behind the liquidity before committing your order. Tape reading methodology in Options Order Flow & Market Maker Positioning.

When you marry this structural awareness with thoughtful use of order types and execution tactics, you turn what is usually a hidden drag on performance — slippage and bad fills — into a controllable, even exploitable, part of your trading process.

Key Takeaways

- Execution quality is a first-class performance variable, not a footnote. In multi-leg options strategies, round-trip slippage can equal or exceed the strategy’s entire expected edge per trade.

- Limit orders are the default. Use market orders only in the most liquid, tight-spread underlyings or in genuine emergencies. Stop orders in options should almost always be stop-limits, not stop-markets.

- For multi-leg structures, use combo orders (all legs as one net-price order). Single-leg execution exposes you to leg risk — partial fills that leave you accidentally naked or directionally exposed.

- GEX and ZGL are your primary regime signals for execution aggressiveness. Far above ZGL in positive GEX: tighter limits, faster fill attempts. Near or below ZGL in negative GEX: wider limits, slower fills, smaller size. Full mechanics in Dealer Hedging Regimes: GEX and ZGL.

- Max Pain is an execution target, not just a strategy signal. Working limits toward Max Pain into OPEX improves fill quality because structural dealer hedging creates real two-sided interest near that level. Mechanics in Max Pain Theory.

- Execute at HVNs, avoid LVNs. High-Volume Nodes in the underlying provide deep two-sided liquidity and reduce impact costs. Low-Volume Nodes (gullies) have thin resting orders; market orders inside LVNs fill at dramatically worse prices. Full HVN/LVN framework in Volume Profile and Auction Market Theory.

- OI concentration identifies the tightest spreads. Strikes with the highest open interest are where market makers commit the most size and maintain the narrowest quotes. OI/Vol relationship in Open Interest vs. Volume in Options.

- Read the tape before the order, not after. Aggressor-side volume on the options tape tells you whether institutional flow is aligned with your intended direction before you pay the spread. Tape reading methodology in Options Order Flow & Market Maker Positioning.

- Always budget for slippage in position sizing. A 1–2% max-loss budget that ignores round-trip spread costs is overstated. Size as if you pay full spread on entry and exit. Dollar-risk framework in Options Risk Management and Position Sizing Guide.